The dust has settled after your car accident. You are dealing with repairs, perhaps some physical pain, and the headache of paperwork. Then, the phone rings. It’s the insurance adjuster. They are friendly, empathetic, and—best of all—they have a settlement figure ready for you.

It is tempting to say “yes” immediately. You want to move on. You want the money in your account so you can fix your car or pay your medical bills.

But pause for a moment. Asking yourself, “Should I accept the first offer from an insurance company for my car?” is one of the most financially important questions you will face this year. The answer is almost always a resounding “no.”

This guide explains exactly why that initial check is rarely the best one, and explores seven compelling reasons why negotiating insurance claims is worth your time and effort.

The Business of Insurance Settlements

Before diving into the reasons, it is crucial to understand the landscape. Insurance companies are businesses. Their primary goal is to remain profitable. While they have a duty to pay out legitimate claims, they also have a financial incentive to minimize those payouts whenever possible.

The first offer is often calculated to be the absolute minimum amount they think you might accept to make the problem go away quickly. By negotiating, you aren’t being greedy; you are simply ensuring you receive the fair compensation you are actually owed.

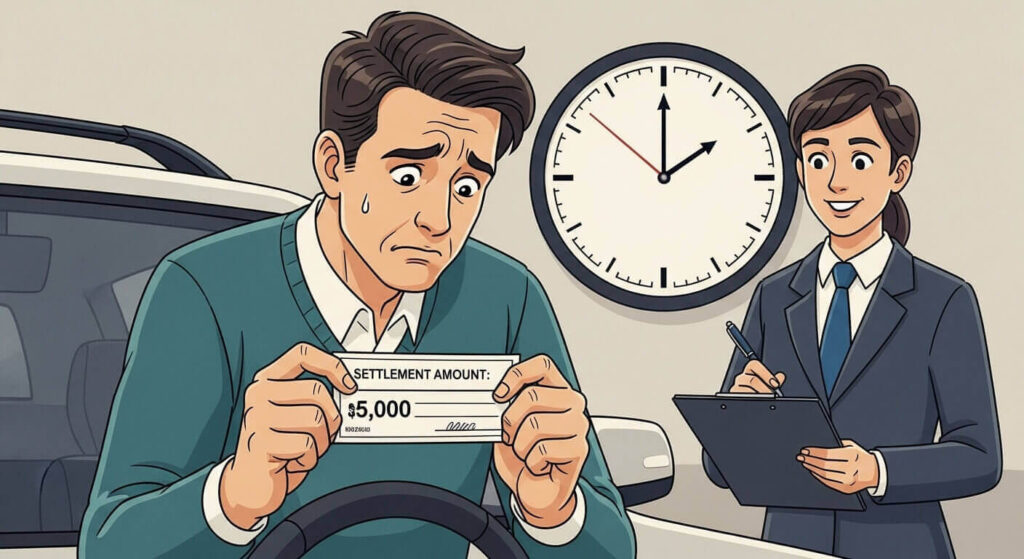

1. The “First Offer” is Often a Test

Think of the first offer from an insurance company like the opening bid at an auction or a garage sale. The adjuster has a range of authority—a minimum and a maximum amount they are allowed to pay for your claim. They almost never start at their maximum.

They start low to test your knowledge and your desperation. If you accept immediately, they have saved the company money. If you reject it, they simply move to the next phase of the negotiation. By accepting the first number, you are likely leaving thousands of dollars on the table that the adjuster was already prepared to pay if pushed.

2. Hidden Vehicle Damage and “Total Loss” Risks

Modern vehicles are complex machines. What looks like a simple fender bender can actually cause structural damage to the frame, alignment issues, or damage to expensive sensors hidden behind bumpers.

If you accept a car insurance settlement immediately based on a visual inspection or a quick estimate, you are signing away your right to ask for more money later. If a mechanic takes your car apart a week later and finds a cracked transmission casing caused by the impact, you will be paying for that out of pocket. Negotiating gives you the time to get a thorough, teardown inspection from a trusted mechanic.

3. Medical Injuries Can Be Delayed

Adrenaline is a powerful masker of pain. Immediately after an accident, you might feel shaken but “fine.” However, soft tissue injuries like whiplash, hairline fractures, or concussions often do not present symptoms for days or even weeks after the crash.

If you settle your claim within 48 hours, you are settling for your current medical state. Once you sign that release form, the case is closed. If you wake up three weeks later with debilitating back pain requiring months of physical therapy, the insurance company is no longer liable. Negotiating buys you the necessary time to ensure your health is stable and all medical costs are accounted for.

4. Initial Offers Rarely Account for “Diminished Value”

This is a critical aspect of negotiating insurance claims that many drivers overlook. Even if the insurance company pays for every penny of the repairs, your car is now worth less than it was before the accident.

When you go to sell or trade in your vehicle in the future, a vehicle history report (like Carfax) will show the accident. This “bad mark” lowers the resale value of your car. This loss is called “diminished value.” First offers almost never include compensation for this. You usually have to specifically ask and negotiate for it.

5. You Haven’t Calculated “Pain and Suffering”

Economic damages are easy to calculate: repair bills, rental car costs, and doctor visits. Non-economic damages, often called “pain and suffering,” are much harder to quantify but just as real.

Did the accident cause you to miss a family vacation? Do you now have anxiety when driving on the highway? Are you unable to pick up your children due to back pain? These are compensable losses. Insurance software algorithms used to generate that first offer often stick to strict math regarding bills and ignore the human cost of the crash. You need to negotiate to humanize your claim and get paid for the disruption to your life.

6. Adjusters Expect a Counter-Offer

You might feel that rejecting an offer is rude or confrontational. It isn’t. It is standard industry practice. Insurance adjusters deal with negotiations all day, every day. They expect you to counter-offer.

When you say, “Thank you for the offer, but based on my research and the extent of the damages, this figure is too low,” you aren’t starting a fight. You are starting a professional conversation. They are often relieved to deal with someone who is reasonable but firm, rather than someone who is emotional. By engaging in the process, you signal that you take the claim seriously and understand the value of your loss.

7. You Might Have Leverage (Like Dashcam Footage)

The first offer is based on the insurance company’s assessment of fault and liability. However, their assessment might be wrong, or at least incomplete.

Perhaps you have dashcam footage they haven’t seen. Maybe there was a witness who can corroborate that the other driver was texting. When you take the time to negotiate, you have the opportunity to present evidence that strengthens your position. A quick settlement denies you the chance to advocate for the true facts of the accident.

How to Handle the Offer

So, the check is dangling in front of you. What should you do?

- Don’t Deposit the Check: In many jurisdictions, cashing the check is legally considered accepting the settlement and closing the claim.

- Request the Offer in Writing: Ask them to send the breakdown of the offer via email or letter. This allows you to review what they are covering and, more importantly, what they are missing.

- Do Your Homework: Gather your own repair estimates. specific to your area. Visit a doctor if you have any physical complaints.

- Send a Counter-Demand: Reply with a higher figure, supported by the documentation you gathered (medical bills, repair quotes, evidence of lost wages).

Conclusion

The moments following a car accident are stressful, and the promise of quick cash is a powerful lure. However, answering “yes” to the first offer is rarely in your best interest.

By understanding these seven reasons to negotiate, you protect your financial future and ensure your vehicle and health are properly cared for. Remember, the insurance adjuster works for the company, but you are the only one who can truly advocate for yourself.

Take the next step: Before you sign any paperwork or agree to a recorded statement, review your policy details and consider getting an independent estimate for your vehicle repairs. If the offer seems drastically low, do not hesitate to consult with a legal professional to understand your full rights.